I promised this a while ago and immediately began to dread the hours and energy it would take to plow through this. :-)

I think I've finally done the work here, though, and can present. So, without further ado, here is a look at my update to Wyatt Emmerich's infamous "Welfare" chart.

Note: for the backstory, read my original blog entry, the New Republic piece and Wyatt's original editorial, wherein he fairly succinctly states his thesis:

"You can do as well working one week a month at minimum wage as you can working a $60,000-a-year, full-time, high-stress job. My chart tells the story. It is pretty much self-explanatory," he wrote.

Indeed.

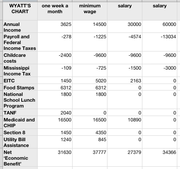

First, his chart, recreated here in my spreadsheet program from the chart that was printed by TNR. (I can't access Wyatt's original because the story link is "printer-friendly" and it's not clear whether the chart made it to the Web.)

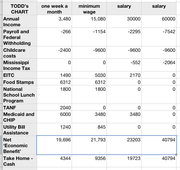

Second, here's my chart.

Here are the footnotes and discussion of the differences:

1.) ANNUAL INCOME. Just nitpicking a bit, but I calculate minimum wage working one week per month as $7.25 * 40 * 12 = $3480; full-time at minimum wage is $7.25 * 40 * 52 = $15080, unless we assume an unpaid vacation. I didn't.

2.) PAYROLL AND FEDERAL WITHHOLDING. The Federal withholding calculated for all four income levels was done by taking 9 exemptions. I got that two different ways -- using an actual w-4 form and using this website (http://www.paycheckcity.com/W4/w4instruction.asp). The 9 exemptions appear to be: 1 for yourself, 1 for your job, 1 for head of household, 2 for each dependent, 1 for childcare credits and 3 for child credits.

This was a critical mistake in Wyatt's original chart; by chosing the family that he did, he managed to maximize benefits on the social safety-net side -- after all, you can't get Medicaid as an able-bodied, working-age adult unless you've got kids and/or are pregnant; you're not eligible for TANF; you don't get school lunch subsidies or as much in food stamps.

However, that same family also maximizes the deductions you get to take, significantly increasing take-home pay for our families with higher incomes, something he didn't take into account in his original chart.

3.) CHILDCARE. Despite the unlikelihood of someone who makes $3480 a year spending $2400 a year on childcare I went with Wyatt's numbers across the board here.

4.) STATE WITHHOLDING. The State exemption for this family, as I read it, would be $12,500, so that's what's reflected. State withholding number also from Paycheckcity.com.

5.) EITC. My numbers agreed with Wyatt's with the exception of the slight difference in income.

6.) FOOD STAMPS/SNAP. I took Wyatt's number here, too. It's worth noting that for this family of three, SNAP benefits are offered (at diminishing amounts) until your income reaches about $23,800 (if memory serves) at which point they drop off completely. I found that odd -- I think I'd support more of a sliding scale. (If someone wanted it, why not offer $60/mo to a parent of two making $29,000... otherwise it could serve as a dis-incentive.) Also note that you don't qualify for SNAP if you or anyone in this family (including the kids) have a COMBINED $2001 or more in the bank. So not everyone qualifies, even if they're low income -- any savings program grandma ever set up for the kids goes to feeding them before SNAP kicks in.

7.) NATIONAL SCHOOL LUNCH PROGRAM. I didn't see any reason to dispute Wyatt's numbers. In fact, the family making $30k might technically qualify for a reduced-price lunch, but I'm not sure how to put that into a numbers, since I can't find how much the reduced-price lunch would be in Mississippi...

8.) MEDICAID and CHIP. This is the big one. Aside from miscalculating the taxes owed (and credits applied) at the top end of his scale, Wyatt's argument is really made here -- he says the net economic benefit of Medicaid is $16,500 for the family of three and he applies that at the two lower income levels, and then cuts that number perhaps to reflect a CHIP benefit for the $30k family.

Two issues:

(1) only the lowest income level may qualify for Medicaid; the full-timer @ minimum wage would only get CHIP in Mississippi

and

(2) insurance for a family of three is a whole lot cheaper than $1375/mo in Mississippi.

Here's the language from Mississippi's Medicaid program: "Adults, who are either parents or custodial relatives, certain degrees of relationship to the children, may also qualify. This is the only program which has both gross and net income maximums." The gross income number is $680/mo; net number is $368/mo.

From the TNR story: "I put the question to [Emmerich], and he told me that he got it by estimating what it would cost the family to buy private insurance on the open market if they did not have Medicaid, applying his own copays and deductible to the equation."

Like TNR, I went to ehealthinsurance.com and looked for a decent plan; low-deductible plans for an adult (I put in my b-day) and two kids was $500/mo. For the two kids alone (emulating CHIP) it was $290 a month. (For the record, I chose the CeltiCare Preferred Select PPO 80/20 Plan.) And, as TNR also notes, salaried professionals generally receive healthcare through their workplace, which is often a group plan and frequently subsidized by the employer. (On the JFP's heath plan through ChamberPlus, covering an employee and one child would cost the employee about $250 per month; based on the rates I assume another child would be an additional $100-120/mo range.)

As TNR pointed out, if you seek not to make the benefit match a reasonable replacement cost but, instead, the actual cost to the taxpayer, Wyatt's argument fares even more poorly; the average cost to the taxpayer for a Mississippi Medicaid recipient is $2510 for the adult and $1659 per child according to the story.

9.) SECTION 8. Add back in Wyatt's number if you want -- I have no idea how he got it. I can't find that on the Internet or in any calculator -- Section 8 benefits are not pegged to income (although you do have to qualify for it), the vouchers are often wait-listed, and I'm not sure how much of a benefit it is to the person who "gets" to live in section 8 or public housing; it's more a benefit to the landlord who collects the subsidy.

And if you do make the assumption that our poor family is getting a Section 8 benefit --based on some reasonable analysis of the odds that they're actually receiving it -- wouldn't it be fair to assume a mortgage interest deduction for our higher-income family?

10.) UTILITY BILL ASSISTANCE. I couldn't find a good place for this number; according to this document at LIHEAP.org (PDF) LIHEAP in Misssissippi only covered 50% of the households actually eligible for the benefit in 2010; the average benefit in 2006 was $469. Eligibility cuts off at around $27k for our sample household.

11.) NET ECONOMIC BENEFIT. I assume I'm calculating this the same way that Wyatt did. See the difference yourself. Wyatt's assertion that someone working one week per month at minimum wage experiences a lifestyle similar to someone making $60k is simply not supported. More interesting, perhaps, is the economic benefit experienced by someone working full-time at minimum wage vs. someone working full-time at $30k. (Note, for the record, though, that both are working full time.)

12.) TAKE HOME - CASH. I added this one. Here I'm taking income, subtracting the direct childcare expenses and paycheck withholding, then adding back EITC and TANF (but not food stamps, since they must be spent under certain circumstances). This is the number that seems like it would be match Wyatt's "disposable income" assertion.

...

CONCLUSIONS:

No, Toto, you don't get the same economic benefit working one week per month vs. making $60k. Or $30k. And the jingle-jangle in your pocket is different at every income level; the more you make, the more control you've got over where and how you spend your money.

What's more, Wyatt's argument really turns on two key numbers (about which he makes some dramatic assumptions) -- healthcare costs and childcare costs.

By putting those in the spreadsheet, it's become very clear to me why these numbers are such political footballs -- and why other countries solve these problems in other ways, particularly single-payer or government-based solutions that use economies of scale to make these things cheaper and more widely available. If Americans weren't forced to play "What If" with those two numbers -- healthcare and childcare -- then THAT might create the stability that Wyatt seeks in order to entice industry back to our shores.

Finally... I didn't attempt to calculate the other benefits that wealthier folks experience, like better (and cheaper) access to capital, more perks at work (401k matches, pension plans, paid leave & vacation, college tuition reimbursement, expense accounts, frequent flyer miles) -- and niceties in our tax code like the mortgage interest deduction. (If our $60k household is paying for a house, contributing to an IRA and perhaps opts for an HSA, they could significantly increase that $40k number.)

I can imagine a world where that family at $60k could buy a house and deduct the interest; borrow against it, get better terms on loans or credit cards, etc., etc., all things that make someone with higher income more mobile and more able to generate wealth. Regardless of the "economic benefit" of social programs, you simply aren't sitting as pretty as someone who is actually making decent money.

P.S. Whew!

Previous Commentsshow

What's this?More like this story

Support our reporting -- Follow the MFP.

Comments

Use the comment form below to begin a discussion about this content.